Corsa Coal Announces Financial Results for Second Quarter 2016

August 10, 2016 – Canonsburg, Pennsylvania - Corsa Coal Corp. (TSXV: CSO) (“Corsa”), a premium quality metallurgical, thermal and industrial coal producer, today reported financial results for the three and six months ended June 30, 2016. Corsa has filed its unaudited Condensed Interim Consolidated Financial Statements for the three and six months ended June 30, 2016 and 2015 and related Management’s Discussion and Analysis under its profile on www.sedar.com.

Unless otherwise noted, all dollar amounts in this news release are expressed in United States dollars and all ton amounts are short tons (2,000 pounds per ton).

Second Quarter 2016 Highlights

- Spot prices for metallurgical coal have risen by over 35% on a year-to-date basis. Corsa has the ability to produce and sell significantly more tons of metallurgical coal over the short term should market conditions continue to improve.

- During the three months ended June 30, 2016, Corsa continued to successfully execute on its fixed cost reduction initiatives. Corsa reached an agreement with an insurer to release certain portions of the reclamation bond cash collateral to fund certain reclamation projects, which totaled $757,000 in the three months ended June 30, 2016. Corsa also successfully renegotiated the transportation contract liquidated damages contract to increase liquidity over the next 18 months and defer the final payment for two years until November 2020. Successful progress has also been made to reduce idle mine expenses, lower capital expenditures, reduce corporate and administrative expenses, lower minimum royalty payments and reduce water treatment costs.

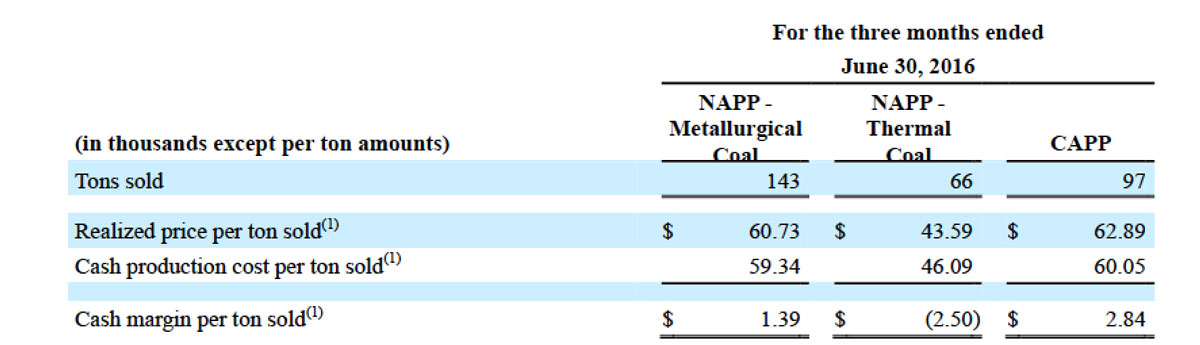

- NAPP variable cost reduction efforts have been successful with the cash production cost per ton sold(1) for metallurgical coal decreasing 11.0% [from $66.66 to $59.34] in the three months ended June 30, 2016 compared to the prior year comparable quarter.

- Corsa’s operations continue to achieve industry leading safety performance, with violation per inspection day rates that are 50% lower than the national average.

- In June 2016, Corsa raised Cdn $3.15 million by way of a private placement of 63,000,000 common shares of Corsa (56,000,000 of which were closed on a brokered basis and 7,000,000 of which were closed on a non-brokered basis) to fund working capital and for general corporate purposes. In connection with the private placement, Corsa also issued a total of 3,360,000 compensation warrants to the lead agent for the brokered portion of the private placement. Each compensation warrant entitles the holder to purchase one common share of Corsa at Cdn $0.05, exercisable for a period of 24 months.

- Key Operating Metrics:

(1)This is a non-GAAP financial measure. See “Non-GAAP Financial Measures” below.

George Dethlefsen, Chief Executive Officer of Corsa, commented, “Spot prices for metallurgical coal are at their highest levels in 2016, and have risen approximately 35% over the first seven months of 2016. Increased Chinese imports, supply rationalization globally, and higher steel demand have served to put supply and demand for low volatile metallurgical coal in balance. This has led to a rise in Corsa’s international sales opportunities both in Europe and Asia, and has pushed domestic pricing higher. We believe the move up in prices has been driven by an improvement in the fundamentals and the stage is set for a continued rise in the second half of 2016. The 5-year downward cycle for metallurgical coal pricing that we have recently emerged from has been the longest and deepest in the last 60 years. We believe that the market has turned the corner and the outlook for metallurgical coal producers has improved.

Despite the upward trend in 2016, metallurgical coal prices remain at levels approximately 70% below their 2011 peak and we remain focused on our fixed and variable cost reduction initiatives. A large volume of April export shipments reduced our average realized metallurgical sales price per ton in Q2, and had a negative impact on profitability. The effect of higher export prices has already been realized in our Q3 shipments and will favorably impact profitability for the remainder of 2016. At our CAPP Division, we have scaled back production levels in response to market conditions for thermal coal. This led to increased costs per ton in Q2 as a result of lower fixed cost absorption. In the months ahead, production levels have the potential to increase based upon ongoing thermal and industrial coal market opportunities.

We are currently focused on growth opportunities, both through organic projects and acquisitions, to build on our existing platform of permitted mines, coal processing infrastructure, mining equipment, and customer relationships. With the continued improvement in metallurgical coal markets, we will actively seek to add to our production and sales volumes through projects with attractive rates of return.”

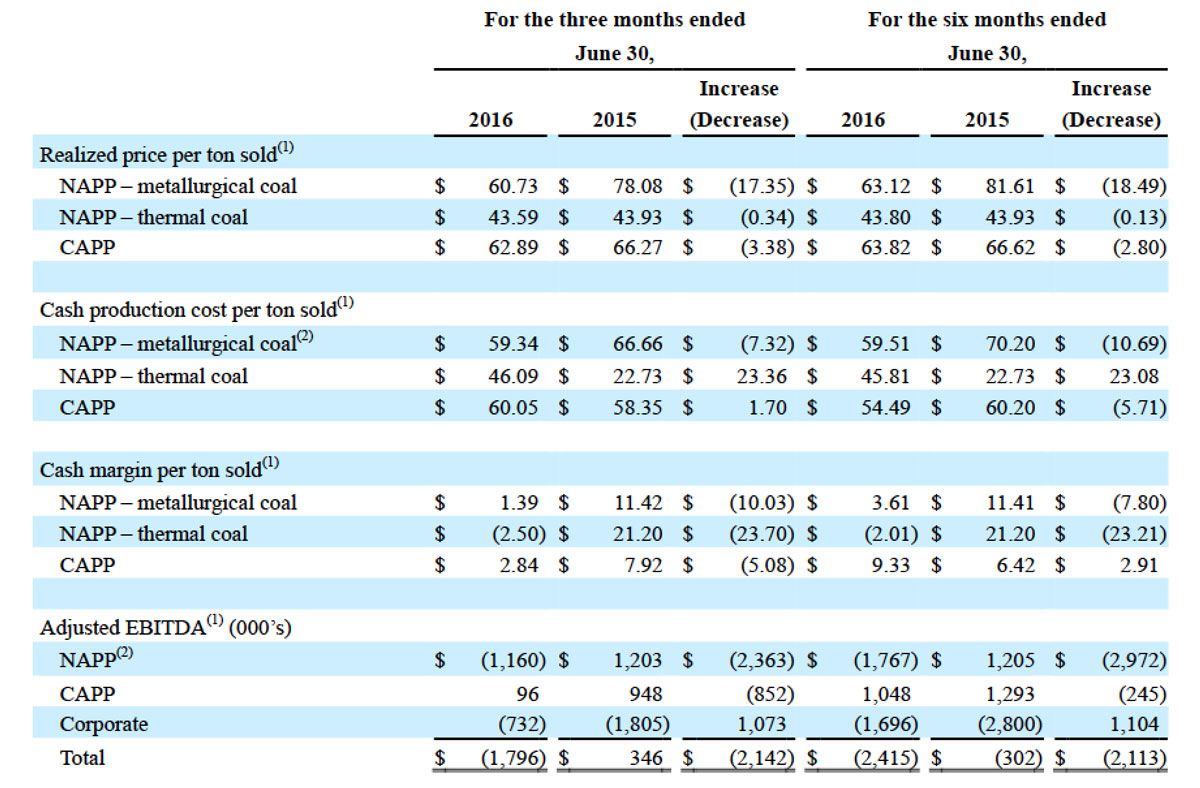

Financial and Operations Summary

(1) This is a non-GAAP financial measure. See “Non-GAAP Financial Measures” below.

(2) NAPP cash production cost per ton sold(1) and Adjusted EBITDA(1) was impacted by adverse geologic conditions in 2016 which increased mining costs.

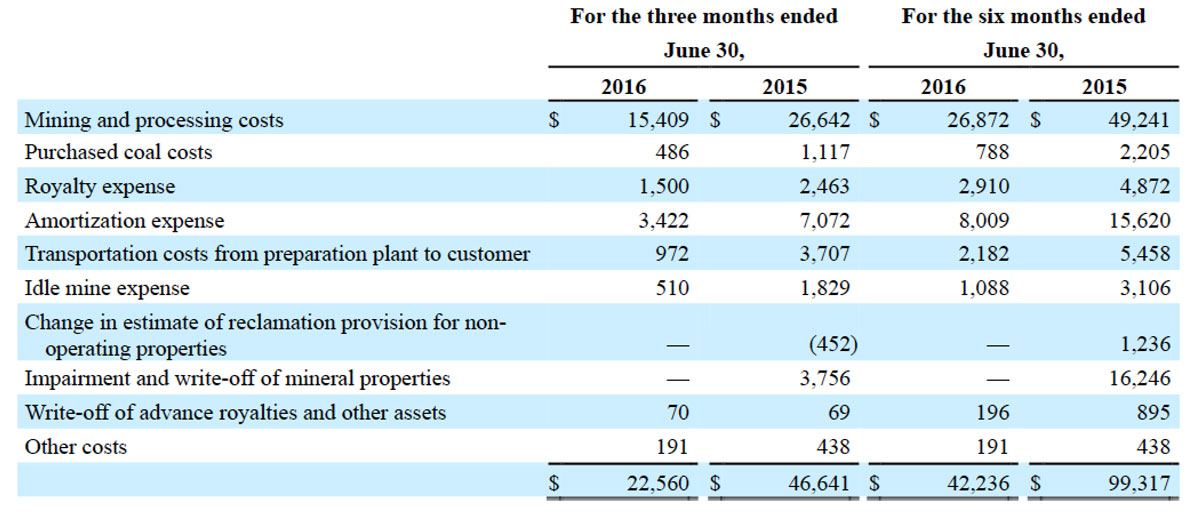

(3) Cost of sales consists of the following:

Guidance

Corsa is updating guidance for the year ended December 31, 2016, from Corsa’s Management’s Discussion and Analysis for the year ended December 31, 2015, which is as follows:

- Updated total sales of 1,350,000 to 1,650,000 tons.

- NAPP Division sales of 850,000 to 1,050,000 tons, including metallurgical coal sales guidance of 600,000 to 700,000 tons and thermal coal sales guidance of 250,000 to 350,000 tons. See “Coal Pricing Trends and Outlook – NAPP Division” below. This guidance remains unchanged.

- CAPP Division sales of 500,000 to 600,000 tons of thermal and industrial coal compared to previous guidance of 675,000 to 775,000 tons. See “Coal Pricing Trends and Outlook – CAPP Division” below.

- NAPP Division cash production cost per ton sold(1) for metallurgical coal of $57 to $62. This guidance remains unchanged.

- NAPP Division cash production cost per ton sold(1) for thermal coal of $38 to $43 compared to previous guidance of $32 to $37 tons as a result of a shift in the timing of a customer contract commencement.

- CAPP Division cash production cost per ton sold(1) for thermal coal of $54 to $59 compared to previous guidance of $56 to $61 tons as a result of a shift of production to lower cost mines.

(1) This is a non-GAAP financial measure. See “Non-GAAP Financial Measures” below.

Coal Pricing Trends and Outlook

NAPP Division

Spot prices for metallurgical coal have risen by approximately 35% on a year-to-date basis as the price of steel has risen substantially, the destocking phase for inventories has ended, blast furnace utilization rates have risen, and imports of metallurgical coal in Asia have risen. In the past three months, weather in China and Australia has impacted production and Chinese initiatives to reduce production of metallurgical coal have been successful. Many metallurgical coal producers have very little supply availability over the coming months, which we believe will lead to further increases in prices. Over the past two years, over 55 million tons of metallurgical coal production cuts have been announced, representing approximately 18% of the annual seaborne metallurgical coal trade. On the demand side, we are seeing increases in steel demand globally, which is leading to very low inventory levels and long wait times for steel orders. This has increased steel prices by over 60% in the United States on a year-to-date basis. Corsa believes that increased infrastructure spending in Asia and the United States will continue to drive steel demand and reverse the decline in crude steel production that was experienced in 2015. We expect these supply and demand factors to continue to provide support for metallurgical coal prices in future quarters.

The third quarter 2016 coking coal benchmark pricing increased to $92.50 per metric ton, representing an increase of approximately 10% from the second quarter of 2016 and is approximately unchanged on a year over year basis. As of July 2016, spot prices have increased past the third quarterly settlement, reaching over $100 per metric ton. If this trend continues, Corsa expects to see a further strengthening in the quarterly benchmark settlement when it is announced in September.

Despite the increases seen in 2016, current metallurgical coal prices remain at levels where a substantial amount of global production is uneconomic. Prior to the upturn in pricing in early 2016, the five-year downturn in metallurgical coal prices represented the longest and deepest downturn in pricing in over 60 years. This situation arose as a result of global producers committing to multi-billion dollar projects in a significantly higher price environment. Large scale mines often take three or more years from final investment decision to first production. New supply came online over 2013 and 2014, a period where demand growth softened. This supply growth is expected to mitigate in 2016 as the pipeline of growth projects is exhausted and prices are insufficient to incentivize new production. Corsa expects that over time, the fundamentals of the metallurgical coal market will rebalance as supply growth ends and production cutbacks are implemented.

Domestically, severe financial distress has caused high profile bankruptcies in 2015 and 2016 and may lead to additional supply cuts in the near future. This situation has also created an environment where producers are deferring capital expenditures, not reinvesting in reserves or permitting efforts, and are highly vulnerable to supply disruptions. For these reasons, Corsa believes that the domestic market is poised to rebound faster than the international seaborne market. Corsa’s geographic proximity to over 50% of domestic coke production capacity and short rail distance and multiple options to access the Baltimore export terminals solidify Corsa’s ability to take advantage of any recoveries in coal pricing.

Corsa’s metallurgical coal sales in 2016 from its NAPP Division are expected to be in the range of 600,000 to 700,000 tons. Approximately 80% of these sales are currently committed at the midpoint of the range. Actual sales will depend on customer demand and market conditions. Vessel nominations for export sales are determined by customers and concluded on a month-by-month basis. Corsa has the ability to produce and sell significantly more tons of metallurgical coal over the short term should market conditions continue to improve.

Corsa’s thermal coal sales in 2016 from its NAPP Division are expected to be in the range of 250,000 to 350,000 tons. Approximately 90% of these sales are currently committed at the midpoint of the range. Actual sales will depend on customer demand and market conditions.

CAPP Division

Current Southeastern U.S. utility market thermal coal spot pricing declined 25% over the course of 2015. As a result, much of the Central Appalachia coal production is uneconomic. Corsa expects utility coal demand for Central Appalachia production to decrease in 2016. Conversely, industrial thermal demand grew 4% year over year for 2015 and Corsa expects industrial demand to grow in 2016.

The CAPP mineral reserve base exclusively consists of high BTU and high carbon content coal. These unique qualities, combined with advantaged logistics, set CAPP apart from other producers and create a niche in the utility and industrial marketplace. As a result, despite thermal supply outpacing demand in 2015, CAPP has been successful in maintaining a high level of contracted sales for the future.

CAPP will continue to target the industrial market segment as it transitions from a utility supplier to an industrial supplier during 2016. The opening of the Cooper Ridge mine has positioned CAPP to service the industrial specialty coal markets. These specialty markets are well suited for CAPP’s coal qualities and relatively protected from natural gas prices and historically reflect higher pricing than the thermal markets.

In response to market conditions and to improve its contract portfolio, the CAPP Division coal sales for 2016 are now expected to be in the range of 500,000 to 600,000 tons. Approximately 85% of these sales are currently committed at the midpoint of the range. Actual sales will depend on customer demand and market conditions.

Non-GAAP Measures

Management uses realized price per ton sold, cash production cost per ton sold, cash margin per ton sold and adjusted EBITDA as internal measurements of operating performance for Corsa’s mining and processing operations. These measures are not recognized under International Financial Reporting Standards (“GAAP”). Management believes these non-GAAP measures provide useful information for investors as they provide information in addition to the GAAP measures to assist in their evaluation of the operating performance of Corsa. Reference is made to the Management’s Discussion and Analysis for the three and six months ended June 30, 2016 for a reconciliation of non-GAAP measures to GAAP measures.

Financial Statements and Management’s Discussion and Analysis

Refer to Corsa’s unaudited Condensed Interim Consolidated Financial Statements for the three and six months ended June 30, 2016 and 2015 and related Management’s Discussion and Analysis, filed under Corsa’s profile on www.sedar.com, for details of the financial performance of Corsa and the matters referred to in this news release.

Caution

The estimated coal sales, projected market conditions and potential development disclosed in this news release are considered to be forward looking information. Readers are cautioned that actual results may vary from this forward looking information. Actual sales are subject to variation based on a number of risks and other factors referred to under the heading “Forward-Looking Statements” below as well as demand and sales orders received.

Information about Corsa

Corsa is one of the leading suppliers of premium quality metallurgical coal, an essential ingredient in the production of steel. Our core business is supplying metallurgical coal with the highest safety, yield, and strength characteristics to domestic steel producers while being a strategic source of supply in the Atlantic and Pacific basin markets. Corsa also offers high heat content, low delivered cost coal to major utilities and industrial users in the Southeast region of the U.S.

For further information please contact:

Kevin M. Harrigan

Chief Financial Officer and Corporate Secretary

Corsa Coal Corp.

724-754-0028

communication@corsacoal.com

www.corsacoal.com

Forward-Looking Statements

Certain information set forth in this press release contains “forward-looking statements” and “forward-looking information” under applicable securities laws. Except for statements of historical fact, certain information contained herein relating to projected sales, coal prices, coal production, mine development, acquisitions, the capacity and recovery of Corsa’s preparation plants, expected cash production costs, geological conditions, future capital expenditures and expectations of market demand for coal constitutes forward-looking statements which include management’s assessment of future plans and operations and are based on current internal expectations, estimates, projections, assumptions and beliefs, which may prove to be incorrect. Some of the forward-looking statements may be identified by words such as “estimates”, “expects” “anticipates”, “believes”, “projects”, “plans”, “capacity”, “hope”, “forecast”, “anticipate”, “could” and similar expressions. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause Corsa’s actual performance and financial results in future periods to differ materially from any projections of future performance or results expressed or implied by such forward-looking statements. These risks and uncertainties include, but are not limited to: risks that the actual production or sales for the 2016 fiscal year will be less than projected production or sales for this period; risks that the prices for coal sales will be less than projected; liabilities inherent in coal mine development and production; Corsa’s ability to make accretive acquisitions and to meet funding obligations; geological, mining and processing technical problems; inability to obtain required mine licenses, mine permits and regulatory approvals or renewals required in connection with the mining and processing of coal; risks that Corsa’s preparation plants will not operate at production capacity during the relevant period; unexpected changes in coal quality and specification; variations in the coal mine or preparation plant recovery rates; dependence on third party coal transportation systems; competition for, among other things, capital, acquisitions of reserves, undeveloped lands and skilled personnel; incorrect assessments of the value of acquisitions; changes in commodity prices and exchange rates; changes in the regulations in respect to the use, mining and processing of coal; changes in regulations on refuse disposal; the effects of competition and pricing pressures in the coal market; the oversupply of, or lack of demand for, coal; inability of management to secure coal sales or third party purchase contracts; currency and interest rate fluctuations; various events which could disrupt operations and/or the transportation of coal products, including labor stoppages and severe weather conditions; the demand for and availability of rail, port and other transportation services; the ability to purchase third party coal for processing and delivery under purchase agreements; and management’s ability to anticipate and manage the foregoing and other factors and risks. The forward-looking statements and information contained in this press release are based on certain assumptions regarding, among other things, coal sales being consistent with expectations; future prices for coal; future currency and exchange rates; Corsa’s ability to generate sufficient cash flow from operations and access capital markets to meet its future obligations; the regulatory framework representing royalties, taxes and environmental matters in the countries in which Corsa conducts business; coal production levels; Corsa’s ability to retain qualified staff and equipment in a cost-efficient manner to meet its demand; and Corsa being able to execute its program of operational improvement and initiatives. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. The reader is cautioned not to place undue reliance on forward-looking statements. Corsa does not undertake to update any of the forward-looking statements contained in this press release unless required by law. The statements as to Corsa’s capacity to produce coal are no assurance that it will achieve these levels of production or that it will be able to achieve these sales levels.

The TSX Venture Exchange has in no way passed on the merits of this news release. Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.